The Napoleon Tax

227 years later, the Government is still taking billions from YOU in tribute…

Enough is enough! Void this claim on your wealth TODAY – with 8 smart moves that could beat the "Napoleon Tax"…

Dear Tax Payer,

Let me take you back to when this financial bloodletting began:

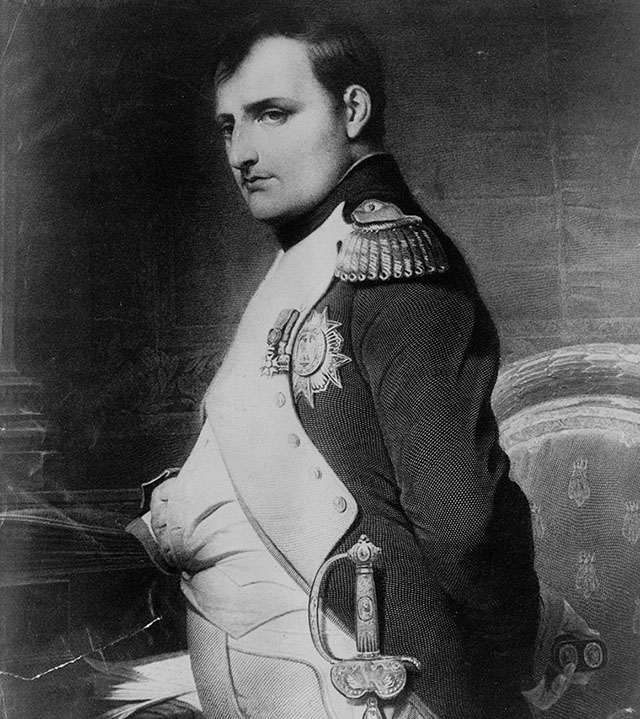

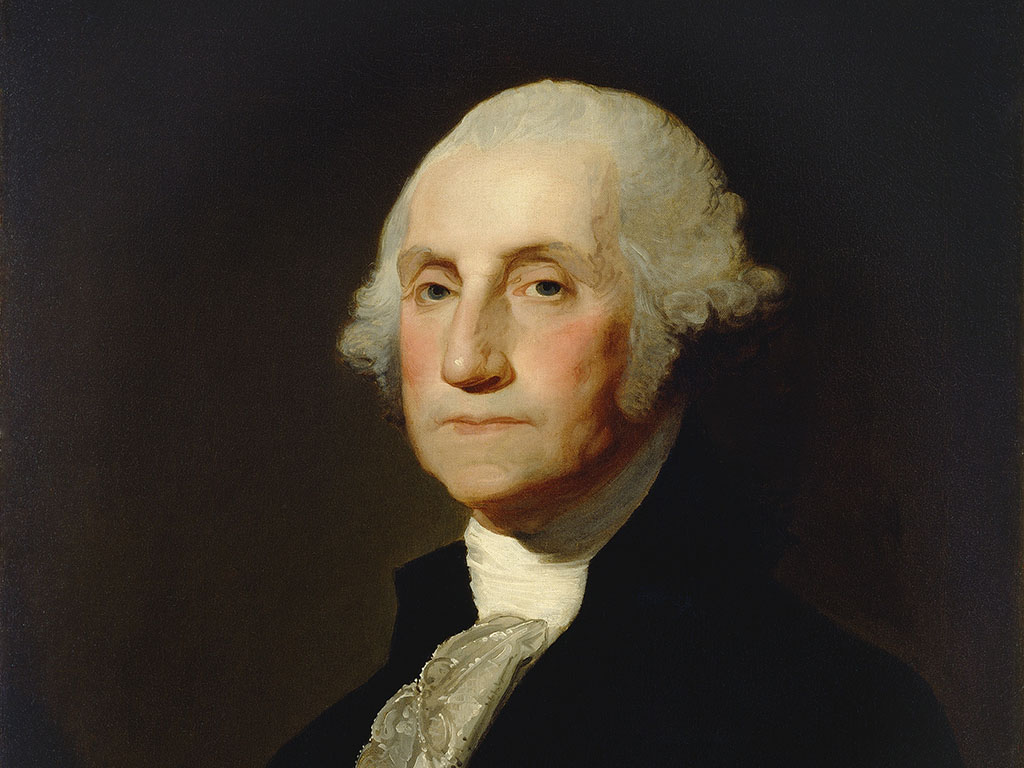

It’s 1796.

Beethoven has just composed Opus 1…

George Washington is in office as president of the USA…

And George III is preparing for war with Napoleon.

To fund the battle against the French Revolution,

the Government passes a controversial new law…

Its purpose:

To harvest the capital of every British citizen that dies…

And leech grieving families of what is rightfully theirs.

This levy is the first of its kind in Britain.

You could call it ‘grave robbing’…

Either way it is a radical new tactic by the Government to foot the cost of a war that would otherwise be unaffordable.

It will pay for the cannons, the gunpowder and the ships that will ultimately help us defeat Napoleon.

But crucially…

It would also make our Government so much money that they would never abolish it.

That’s right…

227 years later, this tax law – that was introduced solely to help us win the Napoleonic wars - is still in existence.

In fact, it’s more prevalent than ever.

As Britain enters “a new era of higher taxes” (FT)…

What is now this country’s ‘most hated tax ’ is hitting record levels.

In June, the Treasury grabbed £795 million from it, the highest monthly total EVER.

And – believe it or not - this is under a Tory government.

Shame on them.

When the Conservatives took power in 2010, the ‘Napoleon Tax’ was wringing £2.38 BILLION from families in mourning.

That figure has risen every single year since then:

By 2020, it was £5.12 BILLION.

Last year, it was up again - at £6.2 BILLION.

This year, between April and July, the government grabbed £2.6bn in just 13 weeks…

Which means this year's takings will likely blow the old record of £6.1BILLION out of the water, shoot past the £7 BILLION mark…

And soar to as much as £8.4 BILLION by the end of 2027.

Napoleon died 202 years ago and yet we’re still paying a tax in his name!

Ask yourself…

Why is a 227-year-old war tax still costing YOU – the British tax payer - billions of pounds every single year?

And the worst thing is…

It’s not only you that is affected by this claim on your wealth…

This affects your children…your grandchildren…their children…and even their grandchildren.

And that’s the thing with the Napoleon Tax…

It punishes your family for your success.

Tell me that doesn’t stick in your craw?

Like most people, you’ve worked hard all your life. You’ve saved properly, paid your taxes and looked after what’s yours.

You’ve done everything you’ve been told to do. Everything that’s expected of you…

So that you can pass on what’s rightfully yours to your loved ones…

And they can benefit from your success, and build a better life for their children.

Quite frankly, securing the financial future of my dependents beyond my time is why I bother to get up early and work hard. Perhaps it's your motivation too?

At least that’s the way it should be.

But more and more people here in Britain are falling foul of this age-old Government tribute which makes that challenge harder.

Make no mistake…

The Treasury will stop at nothing to claim their slice of the pie.

And the penalties can be brutal.

I’ll be honest with you: it gets my back up.

As part of Britain’s longest-running private investment network I want to do something about it.

I want to show you how eight smart moves could beat this 227-year-old assault on your wealth.

And how it's possible to ensure your family LEGALLY sidesteps Napoleon Tax going forwards, beginning today.

But as you’re about to discover…

Unless you keep reading this urgent letter, chances are this could be devastating for you and your family later in life.

The power of private information

Nick Hubble,

Editor and financial strategist

My name is Nick Hubble, by the way.

I’ve seen the inside at Goldman Sachs, and I’ll tell you now…

The system is rigged against YOU.

The government… bankers… fund managers – they’re not in it for you.

They’re in it for themselves – that’s just a fact.

They’ll use you as a means to an end…

Squeezing you for as much as they can to cover their backs on whatever scheme they’re running…

And to collect their fat bonuses, year after year.

It’s one of the reasons why I left my hopes of joining Wall Street behind to become a senior strategist at the British division of an underground, global investment network.

Today I represent an elite club of financial experts and advisors who for 85 years now have been helping private investors like you protect and grow their wealth.

In the past, our organisation has included members of the House of Lords, ex MI5 operatives, multi-millionaire businessmen, former Times editor Lord William Rees-Mogg…

Today the team includes a private wealth guru with close to $1 billion of assets under his management, an investor who knows how to make money…

Plus, the most influential British politician of the last 50 years: a man who knows only too well how the system can work against your financial and personal liberty.

You’ll meet them both shortly.

The club exists for one reason: to study the financial, political and economic world, to understand how that is going to affect private investors, and to share our insight with people like you. People the system foolishly looks down on or ignores.

Our work is certainly appreciated by our readers.

“I know I am with an excellent group of experts giving advice for me to then reflect and make my own decisions. I also appreciate and understand the relevance of the historical perspective and intellect documented of previous major historical events and their overall relevance on today's world. New Investors most certainly try it. It provides independent, forthright information - a sound basis for investment.”

Barbara Ann Facer“It's well written. It's easy to understand. It's not over adventurous and it talks sense”

John Seaman“You have given me the big picture of everything, which Financial Advisors do not discuss – all of the information is valuable to me.”

Glenis KelletAnd today I want to help you legally opt out of having to pay the Napoleon Tax altogether.

Why pay more tax

than you need to?

Believe it or not, there are ways hidden in plain sight to beat the Napoleon Tax.

Of course, the Government doesn’t call it that.

They refer to it as something far more generic.

Something they hope you'll forget about.

But whatever they call it, they’re effectively committing legalised theft, to my mind.

This is something by which they’re taking what’s rightfully yours…

What you’ve worked hard for all your life…

What you’ve set aside for your family in the event of your death…

What could help them benefit from your legacy for many years to come...

And the worst thing is…

They are doing this while your family is in mourning!

What I’m referring to, of course, is:

Inheritance Tax (IHT).

Remember, this was originally introduced to help us fund a war against Napoleon.

And yet 227 years later we’re still being robbed blind!

I want to end that, beginning today.

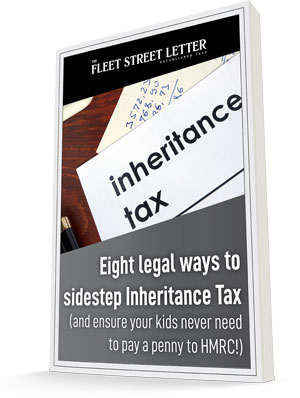

We’ve prepared a special report that you can claim immediately.

It’s called:

Eight Legal Ways To Sidestep Inheritance Tax

And as you can tell from the title, it could help you legally beat this tax altogether.

You might be surprised at what you’ll read in your report.

Chances are you won’t realise that some of these current options are even on the table for you.

And I’ll say now…

There are two things I’d like to share with you that you need to act on immediately.

But keep in mind, when you claim your report:

Everything you’ll read inside is above board and 100% legal. It’s all based on current laws (that could change in future)…

You’ll learn methods of side-stepping inheritance tax including transfers, trusts and various other tax breaks HMRC allows.

Now you might be thinking: ‘how does Inheritance Tax affect me?’

Surely DEATH DUTIES are only the super rich?

For tax dodging oligarchs…

Or creaking, moth-eaten aristos in crumbling estates.

Well, I beg you: THINK AGAIN.

Rapidly rising house prices has pushed more and more homeowners into the Inheritance Tax trap – without many of them realising it.

In fact, given the value of the average UK house price is now pushing £300K, this threshold is extremely inclusive.

You see the means test for your eligibility to pay the Napoleon Tax is set at just £325k.

And that £325k, it includes EVERYTHING you own:

Not just your house…

But your savings, your cars, your holiday home, your stocks and shares, your assets, your art collection…

Literally everything.

It’s all fair game to HMRC. There’s nothing they won’t pilfer.

They’ll claim their slice of the pie – 40% of your entire estate above the threshold – whether you like it or not.

My guess is, your personal estate is way over the £325k threshold.

And remember this:

They are taxing you on money you’ve already paid tax on…

There's nothing wrong with keeping what's rightfully yours!

As I’ve said: you've already paid tax once - do you really want to pay TWICE?

Let’s just say you’re a basic-rate taxpayer, what you’ll pay in tax accounts for around a third of the money you earn.

Around 20% is taken from your income, through National Insurance and PAYE.

But then you get hit with the indirect taxes.

Your council tax likely went up in April.

Yet there still seem to be a lot of potholes, just waiting to shred your car tyres.

And you’ve had to fill up your car more regularly recently, because the train strikes mean you need to drive to work.

More than half of the cost of a litre of fuel is tax - with 36% fuel duty and another 17% of the cost being VAT.

Maybe you like to treat yourself to a bottle of wine to go with dinner.

Well, courtesy of Chancellor Hunt, it went up by 20% in the budget, the largest hike in wine duty since 1975.

And so it goes on.

Which begs the question:

Why should you pay all over again, just because you've worked hard and been successful in life?

Why deprive your family and those who you would like your assets to go to?

The good news is you don't necessarily have to.

With our report you can immediately take charge of the future of your estate and ensure that your wealth is passed on to the people and organisations YOU want.

Eight Legal Ways To Sidestep Inheritance Tax will show you the various loopholes, exemptions and little-known tricks HM Revenue and Customs will allow for legally slashing your tax burden.

- For example, if you are sick of the city rat race; you might be interested in knowing how you can hang up your tie, return to nature – and potentially reduce your tax…

- How, if you are not careful, you could be charged IHT pre-emptively, even though you haven’t died yet!

- And why it pays to be generous when giving your other half gifts

Look, I am not going to list them all here.

You can download the report later and read at your leisure.

It will detail eight moves you can make – and most importantly, explain any criteria and the risks that could be involved with each move.

These are 100% legal exemptions and loopholes you can use to virtually eliminate all of your IHT liability.

As the former Chancellor of the Exchequer Nigel Lawson once said:

“Inheritance Tax is a voluntary tax – you can either do nothing and volunteer (for your beneficiaries) to pay it, or you can take steps to avoid it”.

If you don’t want to be clobbered by HMRC…

If you’d like to leave your wealth to your loved ones…

If you want your nearest to enjoy a legacy, not a tax bill…

You NEED to take steps to avoid it

If you don’t, in the worst-case scenario, it could leave those you care about struggling for money.

Because the taxman wants this money fast.

Whatever your IHT liability is, it needs to be paid to HMRC before your family receives a penny from your estate.

He doesn’t care if those you leave behind are forced to sell the family home… he’ll only wait six months for his money – if it’s not paid by then he’ll start adding on interest.

Take Kathryn Price from Tyne and Wear.

Her father was faced with a bureaucratic nightmare when his mother died two years ago.

“My dad recently had to sort out my grandmother’s estate…

“HMRC demanded an enormous amount of money up front - but most of the money was in shares, which were inflated at the time of death. Soon after, many of these dropped significantly in price, especially the one which was the biggest part of the estate…

“Thing is, a large part of this money overall has been allocated to family members – two of whom have significant learning disabilities. Two teenagers, my daughter and my nephew, who will never be able to earn any money to speak about.

Life is never a level playing field – but is this money really better in the hands of a wasteful, profligate government, or in the hands of those who will be lovingly caring for disabled relatives for the rest of their lives.”

She raises a very good point: why leave your money at the mercy of “a wasteful, profligate government” if you legally don’t have to?

Earlier this year, the government was slammed for wasting £26.8 billion, according to the Independent… with huge sums lost:

“Due to fraud and faulty personal protective equipment (PPE) during the pandemic, poorly-planned defence procurement and on private consultancy fees”.

That’s on top of tax-payer funded debit cards being used to pay for “lavish hotels, furnishings and booze” .

There were even reports of vegan ice cream in Uruguay, hampers from Fortnum and Mason and aqua tots swimming lessons in Panama!

Do you want to see money you have spent a lifetime building… the long hours at work, the effort and sacrifice… spent like that?

Remember, anyone with assets valued at over £325,000 is liable to a whopping 40% tax rate on everything above that threshold. That's £40,000 for every £100,000 of assets - straight to the taxman.

This isn’t something that you can sit back, forget about and just hope it’ll work itself out. That won’t fly.

Your family WILL pay the price, if you fail to act.

But remember too:

You don’t have to put your family through this pain.

You can save them a lot of grief and money at what will be

a stressful and emotional time anyway.

With a bit of planning today, you can legally avoid a huge amount of IHT liability and let those you wish to benefit most from your legacy keep what’s rightfully theirs.

Which is why I am writing to you today.

I want to show you the simple measures you can take to ensure your money isn’t at the mercy of the taxman.

In your exclusive guide, we’ll show you how your family can avoid paying inheritance tax altogether.

In a moment I’ll show you how to claim your copy…

But let me explain WHY I am doing this.

Safeguarding what’s rightfully yours NOW is just the start.

There are ALWAYS ways to protect your money from the clutches of the government and, as you will know after last year’s horror story for global stock markets, our increasingly fragile looking financial system…

As well as the special report, Eight legal ways to sidestep Inheritance Tax, I’d like to start sharing them with you:

85 years of wealth-protection and wealth-building secrets…

As I mentioned earlier, I represent a private club of elite financial experts and advisors who have been helping private British investors protect and grow their wealth – for over eight decades.

We do not publish our work in the City. Nor do we want to.

Instead, we share our research through a little-known, but widely-circulated publication that today I’d like to invite you to join…

It’s called The Fleet Street Letter andit is Britain’s longest-running investment newsletter.

For 85 years now, it has established an incredible track record for helping its readers pinpoint and profit from ‘the news behind the news’ – the threats and opportunities you won’t find published in the mainstream media: until it is too late.

Let me highlight just a few:

In 1938, the founding editor of The Fleet Street Letter, Patrick Maitland, 17th Earl of Lauderdale, spent several weeks in Rome, gathering intelligence on Fascist movements there.

He'd looked into troop movements in Germany. He'd studied Central Power armament plans. And he'd overlaid this against the backdrop of political and economic tension in Europe.

This enabled him to share an incredibly valuable insight with Fleet Street Letter readers: Germany would make war, but not before September 1939.

Germany invaded Poland on 2nd September, 1939.

Maitland looked at the ‘news behind the news’. And found a ‘truth’ that went completely against the official line that ‘appeasement’ would work.

This is what The Fleet Street Letter seeks to do in all its research.

For over three quarters of a century now, this small fellowship of investors have used this kind of information to grow their wealth… no matter what the political, economic or financial climate.

In September 1999, while the world piled into tech stocks, Fleet Street Letter readers received this simple warning: "CRASH IMMINENT." The FTSE peaked four months later, falling into a three-year bear market.

It also predicted the fall of communism, the 1980s property boom and 1987's Black Monday where UK stocks plummeted 27% in a fortnight, and the boom in Taiwanese shares in the mid-90s.

In September 1999, while the rest of the world was piling into tech stocks, they received another warning: ‘CRASH IMMINENT’. The FTSE 100 began its decline four months later.

And when most investors hated gold back in 1999… this group of elite investors were able to quietly position themselves at the beginning of one of the biggest bull markets ever.

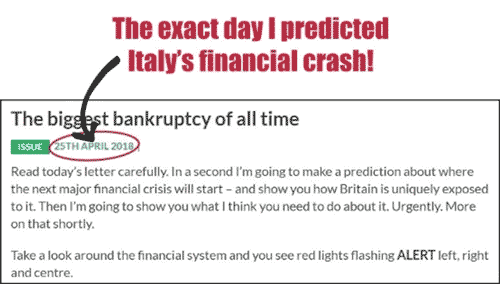

In 2008, readers were discreetly warned that “the City’s dream run is about to end… and it could trigger our worst recession in 35 years.” Five and a half months later Lehman Brothers collapsed and the entire financial sector buckled.

In recent years, you would also have been warned – ahead of time a banking collapse in Italy…

Readers were shown how to shelter their wealth before it triggered one of the biggest drops in UK stocks in a decade - the worst correction in financial markets since 2008.

In 2020 we posed the question: “Is the green bubble little more than ‘investing on thin ice’?”– a year before green stocks tanked.

In 2021, research from our company warned investors that soaring inflation was on the cards – when the Bank of England was still insisting it would stay at 2%... then, at worst, transitory.

We subsequently highlighted the drive for value and dividend stocks… and pointed to the bonds crisis well ahead of Liz Truss’s controversial budget…

Readers have been advised on the delusion of net zero… made aware of the real danger posed by Central Bank Digital Currencies (and what you can do about it)… and the smart way to approach investing in Artificial Intelligence.

Our mission at The Fleet Street Letter is very simple.

- Help you understand what’s coming next in the world of money and markets

- Show you what that means for you, your money and your family

- And share specific investment recommendations to help you protect yourself or profit

We want to arm you with the intelligence and insights to stay one step ahead of the big financial and geopolitical trends shaping your world…

And to show you what to actually DO with your money in light of those trends.

To help you, let me introduce you now to two key members of The Fleet Street Letter team:

First up, giving you his unique insights from the corridors of political power, is probably the most influential British politician of the last 50 years, Nigel Farage.

It matters not one jot if you like him or not, his sense of what is the real story and his fearless ability to ask questions the establishment does not want to hear is unparalleled.

What many people don’t know is that he also understands the world of finance.

His grandfather and father worked in the City. And, having set up an investment club at school, Nigel skipped university and followed in their footsteps.

Aged 18, he joined the world of institutional trading at the London Metal Exchange. First, with the American commodity operation at Drexel Burnham Lambert… then Credit Lyonnais, Refco and Natexis Metals.

As a result, Nigel has incredible connections… amazing experience… and above all, he’s willing to say and predict things that the elite may scoff at… until they come true.

Alongside Nigel, is Eoin Treacy…

You may well have seen him on CNBC, Bloomberg TV, CNN, NDTV Profit or Reuters India. (He has also been interviewed on the BBC World Service, Ireland’s TodayFM and FinancialSense Online).

That’s because Eoin is an award-winning investor with close to $1 BILLION in assets under management.

He currently advises four different $100m funds… manages the money of some of Asia and the Middle East’s wealthiest families… and other clients include sovereign wealth and pension funds.

Past performance is not a reliable indicator of future results.

Most impressive of all, this much sought-after global strategist and wealth manager is the guy other fund managers and traders go to help improve and hone their investment methods. In fact, there are several funds that don’t let their traders on the trading floor until they’ve been coached by Eoin.

Eoin is our Investment Director… the man who turns our INSIGHTS into ACTIONS you can take with your money.

Think of him as your very own $1 billion wealth manager.

Together, they make an impressive team.

And now you can have them working for you because…

Today you can take up one-year’s membership to The Fleet Street Letter – at better than HALF PRICE

Not only will you receive Eight Ways To Legally Sidestep Inheritance Tax…

Within days of receiving the report and following its precise instructions…

You could start to dramatically reduce your tax burden and virtually eliminate all of your IHT liability.

You’ll also get:

- 12 issues of The Fleet Street Letter a year

The financial world moves fast. New trends and threats develop. Old ones die. There’s no one single ‘set and forget’ approach you can take to thrive in the modern financial world.

That’s why our monthly newsletters are so valuable.

They’re your way of staying up to date with the latest thinking, ideas, threats and opportunities.

That might be a new risk developing… a new moneymaking opportunity… a new position for your portfolio. It depends what’s happening in the world.

But whatever IS going on… we’ll be there, on your side and in your corner.

Then you’ll get:

- Full access to the The Fleet Street Letter portfolio

This is what REALLY sets our work apart from the mainstream.

We’re not just here to explain what’s happening.

We translate that into an entire portfolio of investment ideas you can go out and buy to turn that knowledge into action.

An investment portfolio of trading ideas, stock picks and other wealth-building moves is put together for you by a global strategist, trader and wealth-builder with an unparalleled track record...

You’ve already seen Eoin’s credentials.

He is building a mix of long-term strategic positions and shorter-term tactical trades that highlights how you can use your new understanding of the markets to join the dots and gain a practical advantage.

Generally speaking, the recommendations we share with you will involve the stock market. That involves risk – as all investing does.

Some of our recommendations may be listed abroad. That involves foreign currency risk as stocks listed overseas may have the added risk of negative forex movements.

Every recommendation is for your risk capital only – that’s money you can afford to lose.

We’ll explain this to you clearly with every new recommendation.

In fact, EVERY SINGLE idea we share with you will contain a full write up of the risks, the potential rewards, everything.

That’s huge.

Think about it.

You can go pay £700 for a subscription to The Financial Times...

But NOWHERE in those pages of news will you find a single investment recommendation.

It’s all fluff. All noise. It doesn’t matter how many PhDs the editorial teams have. They’re not sharing anything you can ACT ON.

The Fleet Street Letter is different.

You’ll walk away from almost every issue with a fully researched investment recommendation that ties into our worldview.

And here’s the crazy part: though I’d argue we offer far more value, the cost of our work is a FRACTION of the £700 you’d pay for a year of The FT.

In fact, one year of The Fleet Street Letter NORMALLY costs just £249.

That works out at just over £20 a month…

Which is under £5 a week…

Or just 67p a day.

Certainly, our many readers seem to think we offer good value:

“I based my mortgage decision on The Fleet Street Letter’s forecast and it proved to be remarkably accurate.”

Ian Carrington“It's well written. It's easy to understand. It's not over adventurous and it talks sense”

John Seaman“Of all your titles over about 15 years The Fleet Street Letter is my favourite. It does the research that I'd never have time for.”

Colin Byatt“You have given me the big picture of everything, which Financial Advisors do not discuss – all of the information is valuable to me.”

Glenis Kellet“The Fleet Street Letter often provides clear insightful analysis of what is going on behind the scenes in both the political and economic arenas. This is critical information for anybody who wishes to successfully navigate the tricky investment waters of today. Keep up the good work and thank you to all the team”

Glyn WilliamsThey are more than happy to pay the full membership price.

But that’s not what I am going to ask you to pay...

Join today for just £249 £99 a year

Take out a year’s subscription at today’s exclusive new member introductory rate…

And your first 12 months’ membership of The Fleet Street Letter will cost you just £99.

That instantly saves you £150 on the full price of Britain’s longest-running financial newsletter.

Instead of 67p a day, you’ll only be paying 37p.

What’s more, not only will you receive your 12 monthly issues of The Fleet Street Letter…as well as your guide to LEGALLY sidestepping Inheritance Tax…

I will also send you these bonus reports to help you start protecting and even growing your wealth…

REPORT #1: REAL WEALTH: NINE ALTERNATIVES TO THE STOCK MARKET

In this special report for new members like yourself, you’ll discover NINE different ways you can move a portion of your money off the grid…

It includes one of the only investments that: (1) can be consumed, (2) can be sold, (3) performs well, (4) can be held for long enough to survive a financial crash, (4) diversifies your wealth, (5) has a big demand, plus much, much more...

As well as 8 other alternatives to help you shield your wealth out of the traditional system… and into ‘real’ rather than paper assets

After all, you’ve seen what happened to Nigel Farage and his bank

account. It could so easily happen to you to.

As Nigel says:

“It has never been more important to take back control of your money”.

REPORT #2: GOLD 101: THE UNSPOKEN ADVANTAGES

OF A UK GOLD INVESTOR

The authorities are losing their grip.

They can’t balance the books.

They can’t maintain the currency.

Which means you should consider what our fiat currency used to be backed by.

GOLD.

Gold can’t be printed.

It can’t be manipulated.

It can’t be tracked… controlled… distorted… or managed by the state.

Gold is the most stable form of money the world has ever known.

It’s REAL money. REAL wealth.

Throughout human history, there have been thousands of currencies issued by governments.

To my knowledge, they’ve all gone to zero in the end.

This report shows you how to get started buying and storing gold

and other precious metals investments.

REPORT #3: THE ROAD TO FINANCIAL FREEDOM

When it comes to financial markets, everyone seems to be an expert already. Not that they give you the same answer to even the most basic questions… You’re right to be suspicious. And cautious.

It pays to understand the stock market – literally.

This guide will demystify the stock market, teach you how to buy and sell shares, show you how to mitigate risk, lay out how to weigh up any costs involved and show you why investing in the right companies at the right time can completely change your life.

You will also receive two invaluable emails:

SOUTHBANK INSIDER

This is an invaluable email from Southbank Investment Research’s Investment Director, John Butler. And it’s called Southbank Insider for good reason:

John has spent over 25 years in international finance, serving as a managing director for bulge-bracket investment banks on both sides of the Atlantic in research, strategy and asset allocation roles (at both Deutsche Bank and Lehman Brothers).

As such, John has advised some of the world’s largest institutional and private investors on everything from wealth preservation to enhancing returns through a wide variety of innovative strategies, and he has been a #1 ranked Investment Strategist by Institutional Investor magazine. Now he’ll be working for you.*

FORTUNE & FREEDOM

Intelligent insight, in plain English, about the threats to your money and how to avoid them. You’ll get the truth about your money – behind the headlines, jargon and spin.

Totted up, you’ll have unrestricted access to hundreds of pounds worth of valuable financial ideas, wisdom and investment recommendations.*

Best of all, as a new member, you get to kick the tyres on this:

You have a 30-DAY money-back guarantee

Yes, I have arranged with publisher a way for you to try Britain’s longest-running financial newsletter – obligation-FREE.

Think of this as your new member, access all areas pass.

Take the next 30 days to review The Fleet Street Letter.

Check out the reports, the website, the portfolio…

Download and learn the 8 legal ways to sidestep Inheritance Tax…

And if you’re unhappy for any reason, call our member services team within this period, and cancel your membership. You will receive a prompt refund of the membership fee you pay today.

Plus, you’ll get to keep your reports and briefings, whether you decide to stay beyond your 30-day pass or not. A win-win, just for giving us a try.

So, what have you got to lose?

After all, times are tough for you, and your money.

Can you trust the government or the financial services industry to look after you personally?

Or do you need a plan B? An alternative source of advice that has proved itself successful for thousands of investors through the biggest test of all – time.

Today you have the chance to join an elite and rarefied club…

A network of intellectuals and investment veterans who, for over 85 years, have helped private, hard-working Brits protect and grow their wealth…

And if nothing else, can help the Napoleon Tax meet its Waterloo.

Act now, SAVE up to £369 – simply fill out the order form below

I look forward to welcoming you on board.

Best,

Nick Hubble

Editor, The Fleet Street Letter

Important note: Your subscription comes with our automatic-renewal feature. This feature ensures that you will never miss an issue. Currently The Fleet Street Letter renews at £249 per year from your third year onwards. You may opt out of this auto-renew feature at any time after your purchase.

Important note: Your subscription comes with our automatic-renewal feature. This feature ensures that you will never miss an issue. Currently The Fleet Street Letter renews at £249 per year from your second year onwards. You may opt out of this auto-renew feature at any time after your purchase.

By clicking Subscribe Now, you agree to be bound by our terms and conditions, which can be viewed by clicking the link at the bottom of the page

*The Fleet Street Letter subscription comes with a free subscription to Southbank Insider and Fortune and Freedom. These free emails include marketing emails about other Southbank Research products we think you will find interesting. You can unsubscribe at any time by clicking the link at the foot of each email.

Important Risk Warnings:

Advice in The Fleet Street Letter does not constitute a personal recommendation. Any advice should be considered in relation to your own circumstances. Before investing you should consider carefully the risks involved, including those described below. If you have any doubt as to suitability or taxation implications, seek independent financial advice.

General - Your capital is at risk when you invest, never risk more than you can afford to lose. Past performance and forecasts are not reliable indicators of future results. Bid/offer spreads, commissions, fees and other charges can reduce returns from investments. There is no guarantee dividends will be paid.

Overseas shares - Some recommendations may be denominated in a currency other than sterling. The return from these may increase or decrease as a result of currency fluctuations. Any dividends will be taxed at source in the country of issue.

Funds – Fund performance relies on the performance of the underlying investments, and there is counterparty default risk which could result in a loss not represented by the underlying investment.

Bonds – Investing in bonds carries interest rate risk. A bondholder has committed to receiving a fixed rate of return for a fixed period. If the market interest rate rises from the date of the bond's purchase, the bond's price will fall. There is also the risk that the bond issuer could default on their obligations to pay interest as scheduled, or to repay capital at the maturity of the bond.

Taxation – Profits from share dealing, including both capital gains and dividends, are subject to capital gains tax and income tax respectively. Interest received from bonds is subject to income tax.

Capital gains from commodities are subject to capital gains tax. Tax treatment depends on individual circumstances and may be subject to change in the future.

The Financial Conduct Authority does not regulate certain activities, including the buying and selling of commodities such as gold, and investments in cryptocurrencies. This means that you will not have the protection of the Financial Ombudsman Service or the Financial Services Compensation Scheme.

Investment Director: Eoin Treacy. Editor-in-Chief: Nick Hubble. Editors or contributors may have an interest in shares recommended. Information and opinions expressed do not necessarily reflect the views of other editors/contributors of Southbank Investment Research Limited. Full details of our complaints procedure, privacy policy and terms and conditions can be found at, www.southbankresearch.com.

The Fleet Street Letter is issued by Southbank Investment Research Limited.

Registered in England and Wales No 9539630. VAT No GB629 7287 94. Registered Office: 2nd Floor, Crowne House, 56-58 Southwark Street, London, SE1 1UN.

ISSN 0300-4228

Contact Us

To contact customer services, please call us on 0203 966 4580, Monday to Friday, 9.00am - 5.30pm.

Southbank Investment Research is authorised and regulated by the Financial Conduct Authority.

FCA No 706697. https://register.fca.org.uk/.

© 2023 Southbank Investment Research Ltd.

Sources:

- ‘‘New era’ of higher taxes beckons for UK, warn think-tanks” Financial Times, 18/11/2022

- “Government has wasted £26.8 billion under Sunak’s watch, says Labour” The Independent,28/02/2023

- “Scandalous’ Tory government spending on hotels, furnishings and booze revealed” The Independent, 13/02/2023

- “How the Government wasted £14billion of YOUR money (that's enough to pay for all the windfall tax)” Daily Mail Online, 17/11/2022

- “Labour’s mask slips – prepare for huge pension and Inheritance Tax raid if it takes power”Express, 17/03/2023

- “Majority of Britons are ‘against’ Inheritance Tax, Martin Lewis poll suggests” The Telegraph,07/06/2023

- “A guide to Inheritance Tax” MoneyHelper, accessed on 11/10/2023

- “George Osborne pledges to increase Inheritance Tax threshold to £1 million” UK TaxPayers'Allliance, 01/10/2007

- “Inheritance Tax receipts hit record high – how can you reduce your IHT bill?” MoneyWeek,31/07/2023

- “'My dad worked hard all his life – he would have been heartbroken by what the taxman took'”The Telegraph, 31/05/2023

- “‘I’m trapped in my home because of Inheritance Tax’” The Telegraph, 02/06/2023

- “What reliefs and exemptions are there from Inheritance Tax?” Low Incomes Tax Reform Group,31/05/2023

- “How much tax you pay” Which?, 06/04/2023

- “Council tax increases 2023 – how much more will you pay?” MoneyWeek, 17/02/2023

- “The cost of petrol worldwide – why is the UK so expensive?” Arnold Clark, 18/03/2022

- “Wine drinkers hit by biggest single duty hike since 1975” The Wine and Spirit Trade Association,15/03/2023

- “Why Green Stocks Are Falling Despite the ESG Boom in 2021” Bloomberg, 22/12/2021

- “Is Inheritance Tax A Voluntary Tax?” Chester Financial Wealth Management, 27/02/2018

- “Why gold suddenly looks good for investors” Financial Post, 09/05/2023

- “2022 Was One of the Worst Years Ever For Markets” A Wealth of Common Sense, 02/01/2023

- "Inheritance Tax delays can cost beneficiaries dear, writes John McArthur", The Scotsman, 11/07/2018

- "How I lost £165,000 in inheritance tax", The Telegraph, 23/04/2015

- "Revealed: How much tax you'll pay in your lifetime (clue - it's a lot)", The Mirror, 29/08/2016

- "Inheritance tax receipts at record high", The Telegraph, 16/08/2017

- "Number of Britons paying inheritance tax to almost double by 2020", The Telegraph, 19/03/2015

- "United Kingdom House Price Index", Trading Economics, undated

- "Estate and Inheritance Taxes around the World", Tax Foundation, 03/2015

- "Paul Delaroche [Public domain]", via Wikimedia Commons

- "Workshop of Allan Ramsay [Public domain]", via Wikimedia Commons

- “Inheritance tax: a brief history of death duties”, The Guardian, 10/04/2016

- ‘New era’ of higher taxes beckons for UK, warn think-tanks”, Financial Times, 18/11/2022

- “UK in a 'new era of higher taxation', IFS warns”, The Aylmer-Kelly Partnership LLP, 21/11/2022

- “IHT abolition – what happens next?”, RSM UK

- “Government considering cuts toinheritance tax, reports say”, MoneyWeek, 1/10/2023

- “IHT receipts in June highest monthly on record”, Money Marketing, 21/07/2023

- “Inheritance tax receipts UK 2023”, Statista

- “Treasury collects £2.6bn in 13 weeks as IHT receipts rise”, Professional Advisor, 22/08/2023

- “IHT receipts up to £5.9bn with record breaking year expected”, Magma Chartered Accountants, 23/02/2023